When the first motorcars headed onto dusty American roads, time payments were nothing new. Even before the turn of the 20th century, they'd been used to sell pianos and other big-ticket items. The Singer Sewing Machine Company used installment plans to market its merchandise with considerable success, well before the automobile came into prominence. And as they came to be significant for auto purchases, so too did time payments see use for buying jewelry, phonographs ("talking machines"), washing machines, the radios that became available for household use in the 1920s, and so on.

What ultimately became finance companies were originally purchasers of accounts receivable for large or costly household goods, as well as such practical items as farm equipment. Gradually, their business transitioned into automobiles.

When were the first cars sold on time? No one can say with certainty, but there were definitely some such sales by 1905. In 1903, in fact, a Chicago department store made a tentative effort to sell new cars on installment credit, but without much success.

Whatever date is selected for the first installment payments, it's doubtless true that a certain number of private transactions took place earlier.

Installment sales began earlier in Europe – specifically in London and Vienna – than in the U.S. But there, too, time payments were available basically to professional people, and to those with substantial assets.

In 1910, Morris Plan banks began to finance automobile time-payment sales. Especially on the Pacific coast, a number of dealers were offering some form of credit. They gained some popularity in the next few years, but were ordinarily available only to people of substantial standing in the community. Even so, those folks had to pay two-thirds to three-quarters of the selling price as a down payment, signing a note for the balance.

Around 1911, Studebaker began to accept time payments for its E-M-F and Flanders cars, from "responsible buyers." This was one of the first uses of installments by a major automaker, though cars had previously been sold to agents (dealers) on consignment. By 1912, time-payment sales were rather common for commercial vehicles, and some larger dealers offered their own installment plans.

One of the first major financial institutions created specifically for auto installments was the Guaranty Securities Company, formed in 1915 to work with Willys-Knight and Overland dealers. A year later, reincorporated as the Guaranty Securities Corp. of New York, it provided installment financing to dealers for at least 21 car makes.

Bankers and others argued vehemently against the rise of time payments, citing their promotion of extravagance and lack of thrift. They also claimed that more cars were being produced than were needed by the population, a situation exacerbated by time payments.

Although bankers may still have deplored installment sales in the 1920s, others thought them a great boon to the country and the economy. Buying on time would spur people to work harder and be more productive, the proponents thought, and allow families the myriad pleasures of automobility. They argued that if production were slowed down because people were not given an easy means to buy, the economy would falter drastically, and prosperity would have diminished. Their thesis seemed to be: if people are made to want more (of cars and everything else), they will become more productive at whatever tasks they do.

Perhaps the first publicly-claimed plan was initiated in 1914, when a New York City Ford agency advertised cars for $200 down, with monthly notes of $50 each. Around that time, it was possible to go to some Ford and other dealers and pay about half down, signing several notes for the balance, payable perhaps one, two, and three months later.

In 1916, the National Automobile Chamber of Commerce declared the advertising of deferred (time) payments to be "unethical."

Some considered the anti-installment faction to be snobbery: a picture of the wealthy looking down upon the masses who were merely trying to obtain at least a few of the nonessentials (i.e., luxuries) of life. What could be wrong with that?

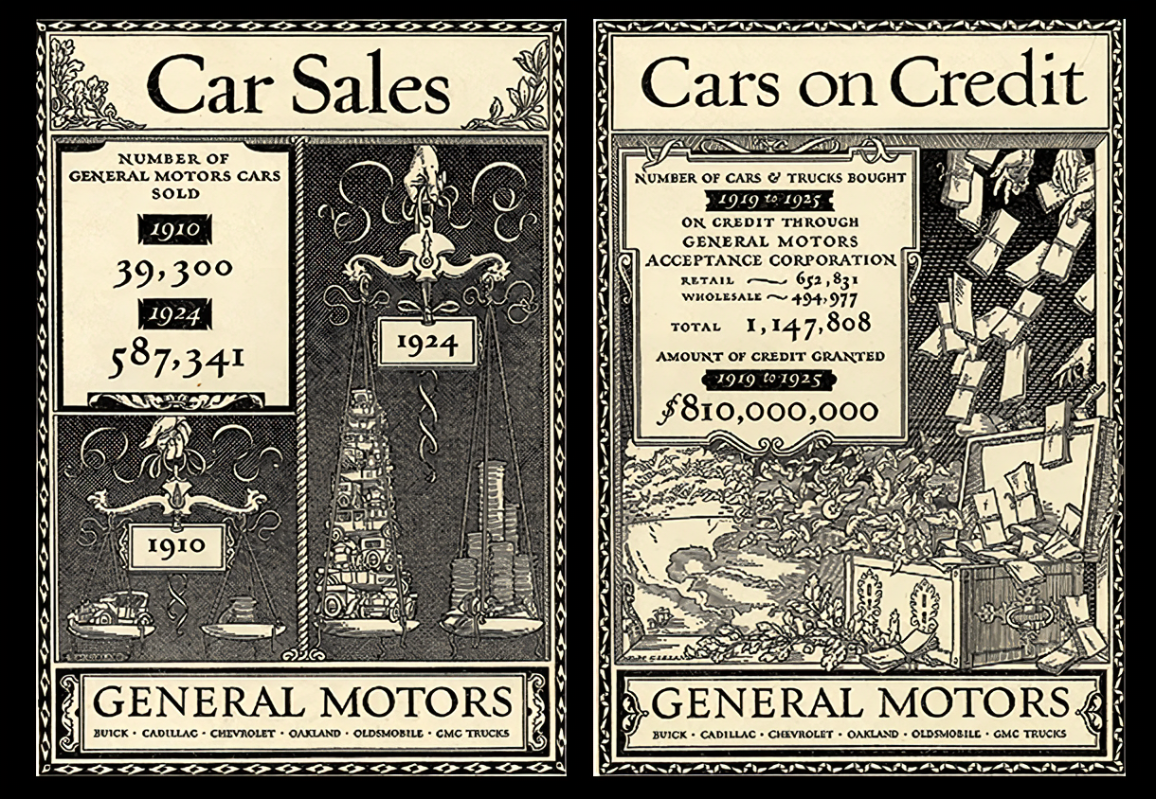

In 1915, Commercial Credit Corp. was handling $17.6 million annually in retail and wholesale paper. General Motors Acceptance Corporation was formed in 1919. In the early '20s, Commercial Investment Trust was established. A 1919 survey of 10,000 GMAC dealers revealed that half of their sales were on credit.

In the spring of 1921, it was estimated that about half of car sales were "on time." By 1923, the figure approached 73 percent; then in 1926, three-quarters. But in 1927, the total dropped to 58 percent of new automobiles, a result of the tighter credit policies instituted after 1925.

Even in the early '20s, installments for passenger cars still were not viewed favorably by most bankers. In 1923, R.E. Olds (then president of Reo) was one of those auto leaders still opposed to installments, which had been adopted by other automakers.

In 1925, Ford experimented with a plan that involved down payments as low as $12.60, with weekly installments of just five dollars. Buyers might have been in for a surprise after a year, though, when their sizable "balloon note" (for the entire remainder) came due. Besides that, a buyer had to have two guarantors whose credit could be investigated and approved. The plan took place in three cities: Detroit, Toledo, and Pittsburgh.

Under the Ford weekly purchase plan initiated in 1923, a customer received a coupon book with which to make $5 weekly payments to the local dealer. Once the total price was paid in full, the car was his. It wasn't exactly time payments in the modern sense by any means, but more than 300,000 Fords were sold that way in a two-year period.

Some observers estimated in the mid-20s that 70 to 80 percent of car sales were made with time payments; and as much as 90 percent of sales of low-priced vehicles.

The high demand for cars (and consequent lower prices) could not, in the opinion of most, have come without installments. Plenty of working people did buy a first car in the 1920s (or '30s), but they could not have done so readily without the availability of used cars – and without installments. However, installments were not nearly so readily available to low-income people then as they would come to be in later years.

By 1924, national financing organizations were insisting on one-third down and one year maximum for new cars. But some local companies were offering terms of up to 18, or even 24, months.

In 1925, according to one source, 68.2 percent of new cars were bought on time. Still, there was some concern about credit being given to working people, expecting them to put a mortgage on future earnings for the dubious desirability of a motorcar. Even so, a full three-quarters of cars – new and used – were being sold on installments. Buy now, pay later was already the economic rule of the land, at least for families that qualified for credit.

In the mid-20s, observers were worried about what they felt were unsound credit practices. Not long before, down payments had typically been 40 to 50 percent; but now they'd been dropping to 33, 20, even a mere 10 percent on new cars. Monthly payment periods had expanded from 8-10 months to as much as 18 months. Thus, the National Automobile Dealers Association and the National Association of Finance Companies agreed on the necessity for requiring one-third down and a 12-month payment period for new cars, or 40 percent and 12 months for used models.

Sometime during the mid-20s, the rather insidious practice of dealers accepting "kickbacks" from a finance company for steering business in its direction began.

Chrysler affiliated with the Commercial Credit Company of Baltimore in 1925. And in 1928, Ford joined with Universal Credit Corp., which was partly owned by Commercial Investment Trust (itself affiliated with several other automakers). These were secret connections, not made public.

In 1929, a typical plan for purchase of a new car required one-third down, with a maximum of 12 months to pay. For used cars, a 40-percent down payment might be demanded, with perhaps 10 months of payments. But economic disaster lay ahead. Specifically, on October 29, a day to become known as "Black Tuesday," the stock market crashed. The Great Depression was about to begin, lasting through the 1930s.

Click here for Overview: Casual History of the Used Car

Click here for Chapter 1: Early Days – Rich Men's Playthings, Poor Men's Dreams

Click here for Chapter 2: Ford's Model T and the Masses

Click here for Chapter 3: Production and Prosperity

Click here for Chapter 5: Family Cars and Family Life

Click here for Chapter 6: Five-Dollar Flivvers

Click here for Chapter 7: Rise and Fall of the Used Car

Click here for Chapter 8: Saturation and Salesmanship

Click here for Chapter 9: A Global Blowout

Click here for Chapter 10: Selling in Hard Times

Click here for Chapter 11: Wheels for the Workingman

Click here for Chapter 12: Okies, Nomads, and Jalopies

Click here for Chapter 13: Motoring in Wartime

Click here for Chapter 14: The Postwar Boom

Click here for Chapter 15: Chromium Fantasies

Click here for Chapter 16: Dealers Face Image Problem

Click here for Chapter 17: Wheels for the Fifties Workingman

Click here for Chapter 18: Teens, Rods, and Clunkers

Click here for Chapter 19: Everybody Drives

Click here for Chapter 20: Personal History of Clunker Ownership